In the wake of the last recession, we saw the explosion in popularity of private label products. People started buying in supermarket chains like Aldi and Lidl. It went from being something you don’t really talk about to getting a sense of pride about finding the best deals.

From our previous Future of Britain research, we saw that there was a clear pick and mix strategy when it came to buying named brands and private label.

To this day, this remains the case. According to Mintel, 78% of people buy both supermarket value own-label and branded products.

According to Mintel, 8 in 10 buyers compare prices between branded and private label products. Meanwhile, half also check to see if there are differences in ingredients. This shows tangibly how shoppers now look for good value, not just low prices and how this ‘savvy’ mindset means that many shoppers scrutinise products closely.

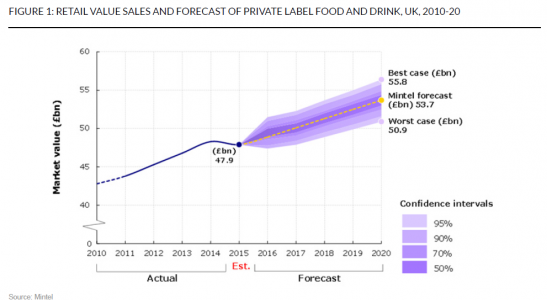

Such consumer behaviour is now ingrained and we have seen that the value of the private label food and non-alcoholic market increased by 12% over 2010-15 to reach an estimated £47.9 billion. This gives own-label a slight lead over brands, with a retail share of 52%.

Forecasts from Mintel always predicted a continued growth of private label over the years:

In a post-Brexit retail environment where consumer confidence is low, this growth of private label could be even stronger than initially anticipated.

Last week began with some big news for generic “store brands,” and the goods in question are not actually being sold in a store, but on a site—specifically, the world’s largest site for retail sales, Amazon.com

The plan is to roll out new lines of private-label brands that will include its first broad push into perishable foods. We have already seen private label products before including toilet paper and batteries, but this is the first plan to sell food (source; Wall Street Journal).

This could have an impact on in-store and online grocery sales, which only accounted for 5.5% of sales in 2015.

Online grocery usage was found to be highest amongst younger consumers, with 55% of those aged 16-34 having done some online grocery shopping in the past year compared to only 42% of those aged 45-64 (source; Mintel online Grocery Retailing, 2016).

So what?

There is an increasing need for brands to differentiate themselves and justify the higher price points versus their private label rivals.

More than ever, communications need to cut through and be relevant to consumers, showing a high understanding of what they need on different occasions. The need to surprise and delight customers is now higher than ever before.

{kind=link}